Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Having a bad credit score can make it difficult to qualify for loans, get into a new apartment, and even find a new job in some industries. On the other hand, a good credit score gives you more options for where you can live and the loans you can get. Figuring out how to improve your credit score fast and implementing a few key changes can help you get your score back on track.

In this post, we’ll look at 14 different tactics you can use to help you improve your credit score and maintain it in the future.

In This Piece:

- Check the Accuracy of Your Credit Reports

- Target the Areas You Need to Improve

- Fix Your Late Payments

- Get Added as an Authorized User

- Clear Any Outstanding Collection Accounts

- Open a Secured Credit Card

- Be Mindful of Your Credit Utilization

- Increase Your Credit Limits

- Set Up Automatic Payments

- Have Your Utilities Reported

- Limit New Credit Card Applications

- Keep Your Oldest Account Open

- Diversify Your Credit Mix

- Negotiate a Lower Interest Rate

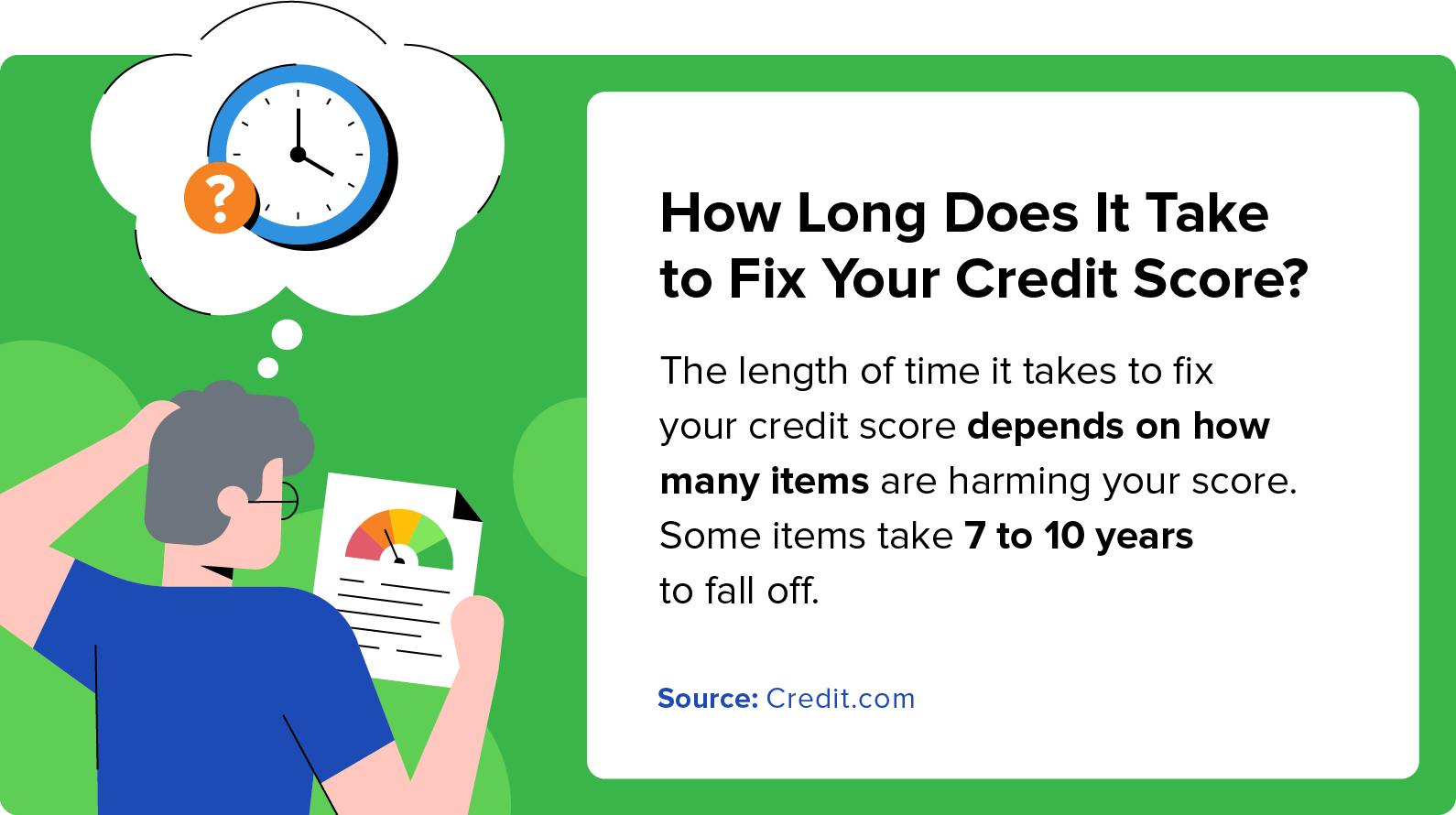

How Long It Takes to Improve Your Credit Score

The exact amount of time it will take to improve your credit score will depend on your unique situation. If your score is low and you’re missing debt payments or consistently taking on more debt, your score can take months or years to improve.

You may be able to increase a low score by as much as 100 points in just one month. If your score is higher or you’ve already started to see an increase after improving your financial situation, you could see the same 100-point increase in six months.

How to Improve Your Credit Score

Wondering where to start? Here are a few tips to help boost your credit score and improve your finances.

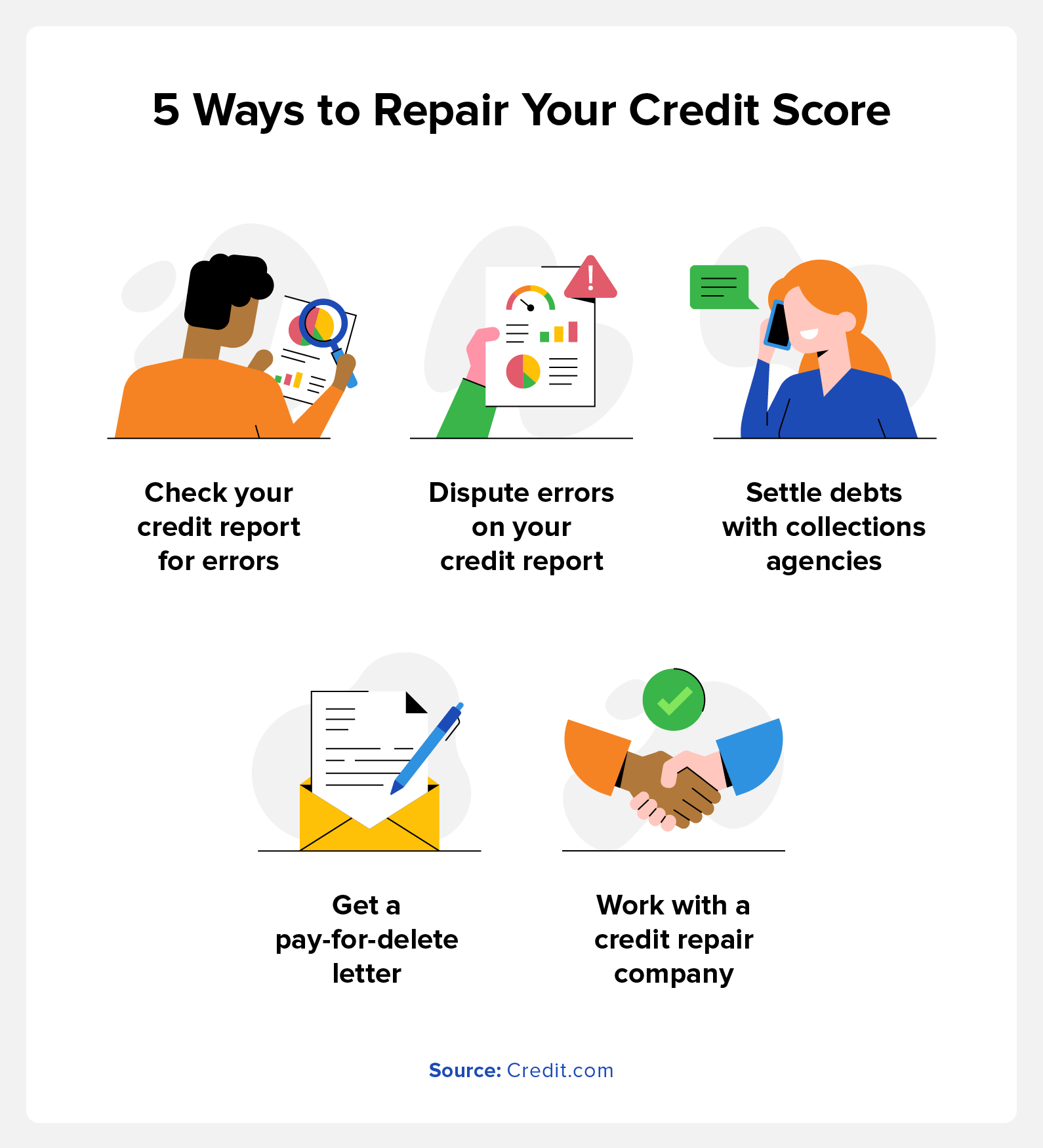

1. Check the Accuracy of Your Credit Reports

Potential impact: If the dispute results in the removal of the derogatory mark, your credit score could increase within a month.

Understanding your credit history and figuring out what’s on your credit report is a great place to start. There are three major credit bureaus, Experian®, Equifax®, and TransUnion®, and each has its own credit report and score based on your credit history. That means everyone actually has multiple credit scores.

Sometimes, you may find errors on your report that you’ll need to correct through a dispute process. If you find an error, you’ll have to file a separate dispute with each credit bureau since they’re run separately. If there are multiple errors on your credit reports, you’ll need to dispute each of those individually. Removing errors can be one of the fastest ways to boost your credit score. Every derogatory mark on your credit report could cause your score to drop, and removing those marks gives your score a chance to improve.

You may also be able to dispute credit inquiries on your report, many of which are hard inquiries and can impact your credit score. A hard inquiry stays on your credit report for an entire year.

While each individual hit is relatively small, it can push you over the edge from one credit score tier to one below it. What’s more, several hard inquiries over a short period can drop your score by as much as 10 points.

If you didn’t approve the inquiry into your credit, you may be able to get it removed. This could potentially increase your credit score, but only slightly.

2. Target the Areas You Need to Improve

Potential impact: You’ll gain a clear understanding of where your credit score falls so you can build a strategy to help you boost the score over time.

Checking your credit reports from each of the three main credit reporting agencies is easy. Under the Fair Credit Reporting Act, you have the right to obtain a free copy of all three credit reports once each year. You can access free copies of your report with each of the three bureaus through AnnualCreditReport.com. You can also check your credit through our free credit report card, which provides a snapshot of your credit and a letter grade for each of the factors that drive your score.

Once you receive a copy of your credit report, you will know which areas need improvement and where to start.

3. Fix Your Late Payments

Potential impact: Removing late payments from your credit report could cause your score to increase.

Late and missed payments can stay on your credit report for seven years. These derogatory marks lower your credit score and make you appear as a bigger risk to lenders.

Credit reporting agencies don’t remove these items, but you may be able to convince a creditor to do so. Creditors may forgive one late payment if you have a history of on-time payments. But you’ll need to call and discuss it with them. Removing repeated delinquencies may require a little more effort on your part.

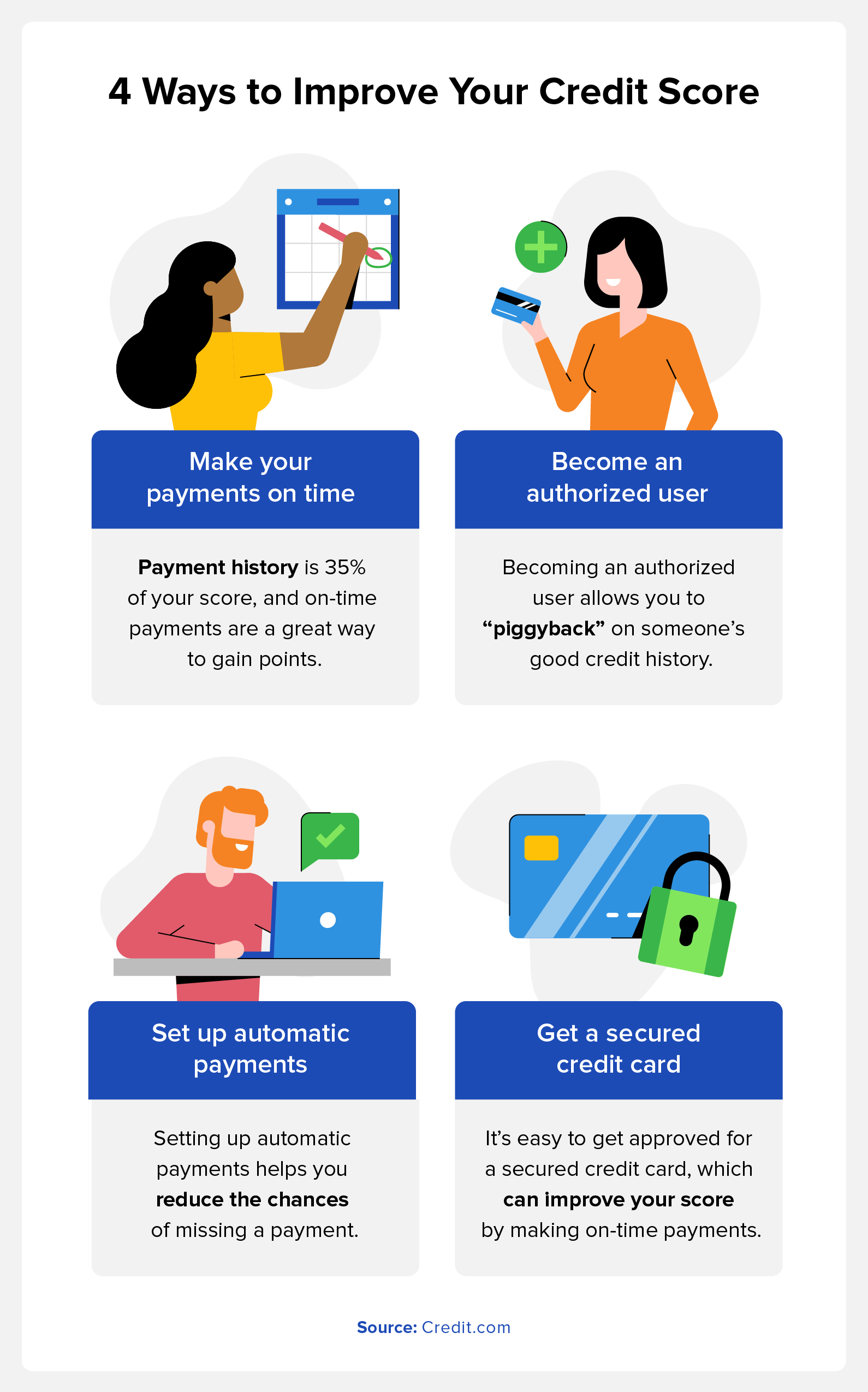

4. Get Added as an Authorized User

Potential impact: As long as you and the primary cardholder stay current on payments, you’ll likely see an increase in your credit score.

You can become an authorized user for a credit card account if you have a friend or family member with a good credit history. Even if you don’t use the credit card, your credit reports will leverage the person’s credit history of on-time payments, which may help you boost your score.

This is also known as “piggybacking” on someone’s credit. Should you do this, it’s important to remember that the other person and yourself are now linked. This means that using the card and missing payments can harm the other person’s credit score and vice versa.

5. Clear Any Outstanding Collection Accounts

Potential impact: Once the debt is removed from your credit report, your score will likely increase. The extent of the increase will depend on how much debt you have.

Contacting your creditors about paying off your debt is a great way to raise your credit score fast. Make sure they agree to remove the negative hit to your credit report if you repay it in full—and get it in writing. If this agreement isn’t made, there will likely be no impact to your credit.

After making an agreement with the collections company, request a pay-for-delete letter to have it removed from your credit report. A pay-for-delete letter is an agreement in writing stating that the creditor will have the derogatory information removed from your report.

6. Open a Secured Credit Card

Potential impact: Making full, on-time payments can help you boost your score. Payment history makes up 35% of your FICO score, and those on-time payments can help you build your score quickly.

Having and using a credit card can help you build credit, but it’s difficult to get approved for a credit card when you have a low credit score, which is where secured credit cards become useful. Unlike a typical unsecured credit card, where you are given a credit line based on your credit alone, you can open a secured credit card by depositing money, which becomes your credit limit.

For example, if you deposit $500, you will have a $500 line of credit. Banks are more likely to approve you for a secured credit card because it’s less of a risk. Your payments on this card are reported to the credit bureaus, and if you make those payments on time, this can help you raise your credit score.

7. Be Mindful of Your Credit Utilization

Potential impact: Your credit utilization makes up 30% of your credit score. By reducing what you owe, you can increase your score over time.

Your score can suffer if you carry a large amount of debt compared to your available credit. Credit utilization accounts for 30% of your credit score. So, if your total available credit on all of your credit cards is $10,000, and you’re currently using $8,000 of it, paying down those balances can increase your score by decreasing your total credit utilization.

Experts recommend keeping your credit utilization ratio at around 30%. Using the above example, this means keeping your total credit card balance at $3,000.

8. Increase Your Credit Limits

Potential impact: Your credit limit impacts your credit utilization ratio. A higher limit will lower your ratio, positively affecting your credit score.

As discussed above, a low credit utilization ratio is ideal, and increasing your credit limits is one way to improve your credit utilization.

Using the same $10,000 example, $4,000 of debt would be a 40% credit utilization ratio. If you increase your credit limit to $15,000, that same $4,000 debt would only be 26%. But keep in mind that this could trigger an inquiry and will also impact your score.

If you want to increase your credit limit, you may need to contact your credit card issuer. Let them know that you’re interested in increasing your limit. They’ll review your payment history, credit score, and current credit utilization ratio to determine if a rate increase is appropriate.

9. Set Up Automatic Payments

Potential impact: Automatic payments will help you reduce the risk of late or missed payments, improving your payment history. This could improve your credit score.

Having a good payment history is one of the best ways to improve your credit score because your payment history accounts for 35% of your FICO® score. One of the simplest ways to do this is to set up automatic payments. Simply go to your credit card company’s website, make an account, and set up automatic payments for the minimum each month.

This way, you never have to worry about forgetting your payment. You can also make additional payments during the month if you plan on paying more than the minimum.

10. Have Your Utilities Reported

Potential impact: Reporting additional on-time payments could help you improve your credit report’s payment history. This may increase your credit score over time. The lower your score is, the bigger the credit score increase you may see.

Typically, your utilities are not reported to the credit bureaus, but adding your payments on time each month can strengthen your credit history and positively impact your credit score. You may be able to get your utility payments added to your credit history by using different services like Credit.com’s ExtraCredit® service.

11. Limit New Credit Card Applications

Potential impact: By reducing the number of hard credit inquiries on your credit report, you can maintain your credit score even if nothing changes. Your score could increase if you make payments and reduce your total debt.

The more credit cards and loans you apply for, the more hard credit inquiries you’ll have on your credit report and the more your score could drop. Instead of applying for loans and credit cards whenever you think you’ll get a good deal, only apply for new lines of credit and loans when you know your score can handle the hit.

This is even more important if you’re trying to figure out how to build credit to qualify for financing for a new home, car, or other larger purchase. When you open a new credit card or take on a new loan, your credit score will drop, and your credit utilization ratio could go up. This could make qualifying for a new home loan or car loan harder when you need one.

12. Keep Your Oldest Account Open

Potential impact: Holding on to older accounts preserves your credit history, which prevents your average age of credit from negatively affecting your credit score.

Credit history length, or the age of your oldest credit account, is worth 15% of your FICO score, and the older it is, the better. Rather than closing out a credit card you don’t use often, keep the account open as long as you can. This will increase the average age of your accounts, which can help you keep your credit score higher.

Remember that many credit card issuers close accounts for lack of activity. To keep your account open, consider using that old card for small monthly purchases and pay them off in full. You could also use the card to pay for recurring subscriptions like a streaming service and set up automatic payments to ensure you pay the balance in full each month.

13. Diversify Your Credit Mix

Potential impact: By taking on different types of debt, you’ll improve your credit mix, which makes up 10% of your FICO score.

Credit mix refers to the different types of credit accounts you have associated with your credit report. Your total credit mix makes up about 10% of your FICO score, and the more diverse that mix is, the better your score could be. If possible, you’ll want to have both revolving credit accounts and installment credit accounts:

- Revolving credit accounts: These lines of credit are ones that you can use repeatedly as long as your total balance is lower than the credit limit on the account. It includes credit cards, home equity lines of credit, and personal lines of credit. If you max out the line of credit, you won’t be able to use it again until you pay it off at least a little.

- Installment credit accounts: These lines of credit are ones that you can typically use only once. You receive a lump sum from your lender and must pay it off in full by the end of the repayment term. It includes mortgages, student loans, auto loans, and personal loans.

By having more than one type of credit account on your credit report, lenders can better understand your finances and see if you’re responsible when using those accounts.

14. Negotiate a Lower Interest Rate

Potential impact: Negotiating a lower interest rate could help you pay off your debt and lower your credit utilization ratio, potentially boosting your score.

You may be able to negotiate a lower interest rate with your credit card issuer by speaking with them and requesting a rate reduction. If awarded, that lower rate could help you pay off what you owe faster.

Lower interest rates can reduce your payments by reducing the interest you owe on your card balance each month. But if you keep making the same monthly payment you were before negotiating a lower interest rate, you could pay your card’s balance off faster. And when you pay off that outstanding balance, your total credit utilization ratio may decrease, further boosting your credit score.

How Your Credit Score Is Calculated

When working on improving your credit score, it’s helpful to know how your score is calculated so you know which factors are the most important. You can then make a plan for where you should start. Here are the major credit scoring factors and how each one can impact your credit score:

- Payment history: A history of overdue and missed payments may signal that you are a bigger risk to creditors. Thus, this factor has the greatest negative effect on your credit score, making up about 35%.

- Amount of debt: Debt is 30% of your FICO Score and also weighs heavily on other credit scoring models. This is also known as your “credit utilization,” and ideally, you want to keep it below 30% of your max credit limit.

- Age of accounts: Creditors like to see a proven record of borrowing, utilizing, and repaying credit. If you’re new to credit and borrowing, there isn’t a lot of data to go on. This makes up 15% of your score.

- Account mix: Making 10% of your score, lenders want to make sure you can handle both revolving and installment credit. This means credit cards that you continue to use after repaying and loans that are closed upon full repayment.

- History of credit applications: Multiple hard inquiries on your credit may look to lenders like you are overextending yourself financially. This will lower your score. Credit inquiries make up 10% of your score.

How to Improve Your Credit Score FAQ

Below, we’ve answered some of the most common questions people have about how to quickly improve their credit score.

What Is the Fastest Way to Boost Your Credit Score?

The best way to improve your credit score quickly is to pay down your outstanding balances. If you can’t pay off your credit card in full, try to make more than the minimum payment on each credit card and loan you have. The lower your balance is, the more your score may improve.

How Long Does It Take to Rebuild Credit?

Everyone’s credit and financial situation is different, and the amount of time it will take to rebuild your credit can vary. If you’re taking on more debt and aren’t paying off your balances, it may take longer to rebuild your credit. But if you make more than the minimum monthly payment on your debts, only open lines of credit or take on loans that you truly need, and keep older accounts open, you may be able to rebuild your credit faster.

How Do You Improve Your Credit Score When You Have Collections?

If you have accounts in collections, requesting a pay-to-delete agreement with your creditors could help you boost your score. This agreement removes the derogatory mark on your credit report once you pay off the balance in full. Without that derogatory mark on your credit report, you’ll likely see an improvement in your credit score.

What Is a Good Credit Score?

A good credit score typically falls around 700 and higher, depending on the type of score you’re looking at. The higher your score is, the easier it will be to qualify for new loans, credit cards, and other products.

Take the First Step Toward Improving Your Credit Score

Your credit report is the best place to start if you want to improve your credit score. Your credit report will show you your account balances, any derogatory marks you may have, and hard credit inquiries. This will help you see where to start, and you can also find out if there are any errors on your credit report.

To get an idea of where you stand with your credit, get your free credit report card today.

You Might Also Like

You probably know credit bureaus keep credit reports. But did you... Read More

March 7, 2023

Credit Repair

[Disclosure: Lexington Law Firm advertises on Credit.com an... Read More

March 6, 2023

Credit Repair

Your credit history and the scores based on it are important fina... Read More

May 10, 2022

Credit Repair