It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published March 4, 2021

Even if you have a little bit of debt, you need to find ways to manage it properly. Whether you’re paying off your tuition, loans, or credit card bills, this guide has been designed to help you better manage your outgoings and gain a better understanding of the options available.

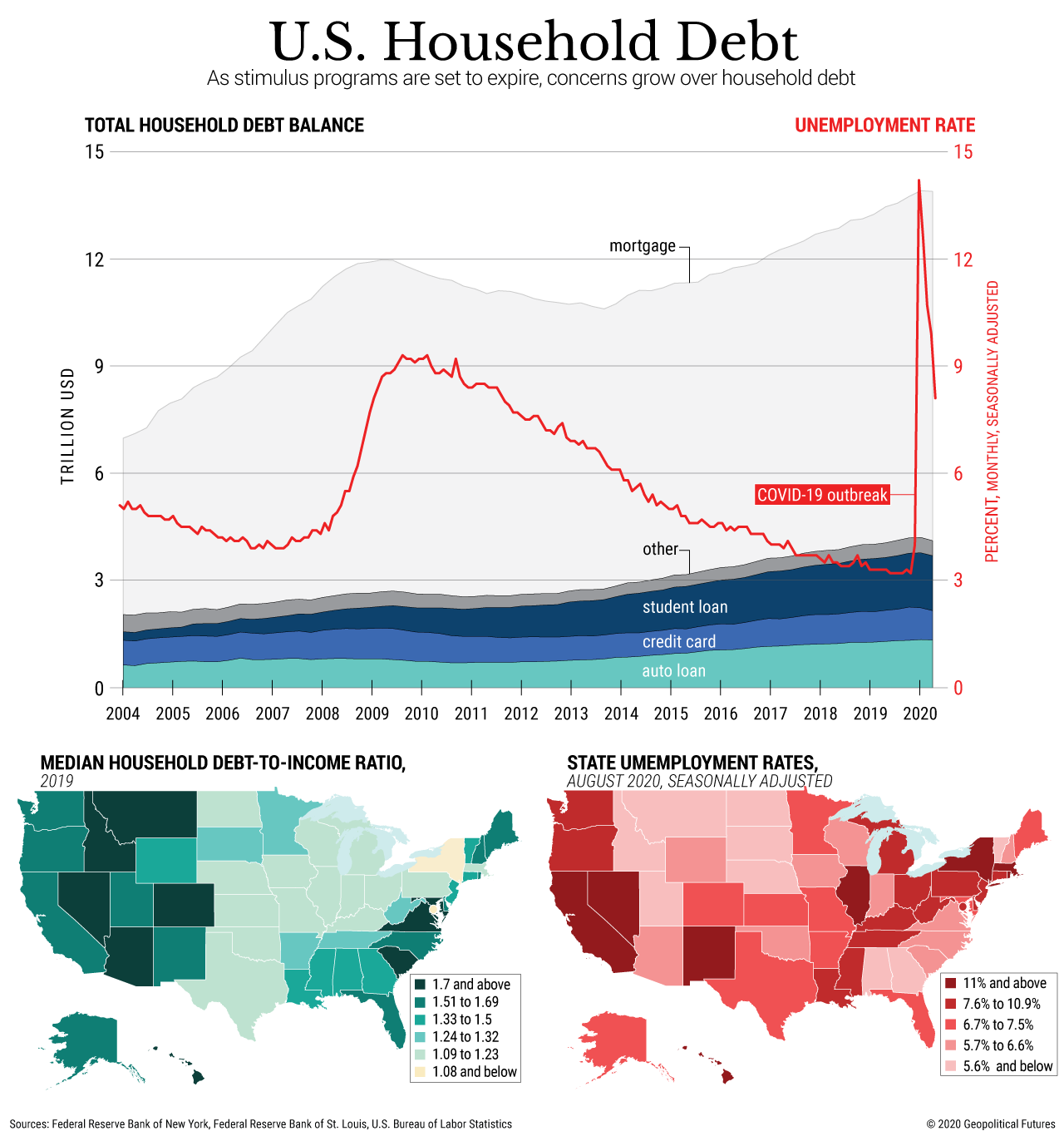

Since the COVID-19 pandemic, a sharp spike in unemployment levels has prompted talk of an emerging debt crisis in the US.

(Image: GPF)

As Coronavirus began to take hold, household debt in the US peaked at over $14 trillion, mostly consisting of mortgages and student loans, alongside credit card debts. With unemployment peaking significantly higher than that of the financial crash of 2008, there may be more of us than ever staring at financial hardship in the coming months and years. However, the following tips may help to better manage your debt and steer clear of the choppy financial landscape.

It may seem like an obvious point to begin with, but the most significant step you can take is to review your financial outgoings. Record your spending in a diary–whether it’s a physical one or a mental one–and take into account your recurring purchases. This will help when it comes to eliminating unnecessary spending habits.

Consider making small changes to your everyday spending. These alterations may not seem to make a significant difference, but expensive habits can quickly add up. And they can make a significant difference come payday.

Sticking to budgets can be a great way of better managing your outgoings and incomings to better take care of your debt. Find a debt management app to help you to work out where your money goes each month and organize how much is left over once your bills have been paid.

By reassessing your various outgoings, it’s possible to come up with a recurring sum of money that can go towards monthly debt repayments.

Use a bill payment calendar to help you work out which debts you can pay off each month. This tool is great for keeping track of the size of debts that you have and arranging how each amount owed can be addressed.

For example, if your payday is on the 25th of every month, it’s possible to use the same calendar each month to pay your bills. If your payday falls on different days, then simply create a new calendar on a monthly basis.

Make sure you prioritize paying your urgent debts first. Although you could clear a series of small debts in one go, the impact of not paying up on a large debt may have more significant ramifications for your home or possessions.

Likewise, however, you may have large debts that have more lenient due dates attached. If you have multiple accumulated debts, order them in terms of the severity of missing their payment dates.

You might need to contact priority creditors if your situation is more urgent, like if there’s a real danger of you being involved in an eviction. Be sure to let your creditors know that you’re looking for debt advice and aiming to find a satisfying resolution for all parties.

Debt consolidation loans help you to merge your different debts and pay them off through the help of a single loan–usually alongside more manageable monthly payments. This means that all of your debts can theoretically be rolled into one single lender.

If you’re struggling to keep on top of your debts, it’s important to consider whether you’ll manage to keep up with the terms of your new loan. Always look to take debt advice before making any decisions that you’re unconfident about regarding consolidation loans. Consult a debt advice organization to check out the potential for utilizing the help of a debt consolidation loan.

The idea of having more outgoings may seem like the last thing you need right now. However, registering with a micro-investing app could be an efficient way to save small amounts of spare change to ultimately use to pay off accumulated debt.

The way micro-investing works is that apps can automatically round up your daily purchases to the nearest dollar and invest the difference on your behalf. This means that a small amount of your spending can be placed in a virtual piggy bank to use later on.

Even if you’re only registering $10 per week in your micro-investing account, that could ultimately contribute $520 at the end of the year towards paying off your debts. And this makes little to no change to your lifestyle.

If it feels like your debts are getting on top of you, don’t panic, there will always be options available–even if you feel like you’re being buried in a pile of payment demands.

If you don’t have the money you need to pay off your debts, you may have to make the difficult decision to file for bankruptcy as a means of clearing the debt you owe. Of course, this process has serious consequences for your financial status and any future credit that you wish to take out. But it can help to pave the way for a fresh start. So, it’s important to remember that this option should only be considered as a last resort.

It’s important to know that no matter how bad your debt becomes, there’s always someone that you can talk to and share your problems with. Sharing your problems with family and friends won’t make them go away, but it helps you to gain a fresh perspective on your position. Of course, there will always be professional support available if you need it too. Nobody should ever have to suffer in silence.

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.