It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published November 22, 2024

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

A personal loan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects.

Most people don’t have $5,000+ sitting in their bank accounts to spend on emergency car repairs or take advantage of a great deal on their dream vacation. That’s where personal loans come in. Just like a mortgage or auto loan, personal loans allow you to cover large purchases or expenses under the terms that you'll pay the loan over time, typically with interest.

If you’re considering taking out a personal loan, here’s all you need to know to ensure you’re making the right money moves to fund your future investment.

Key takeaways:

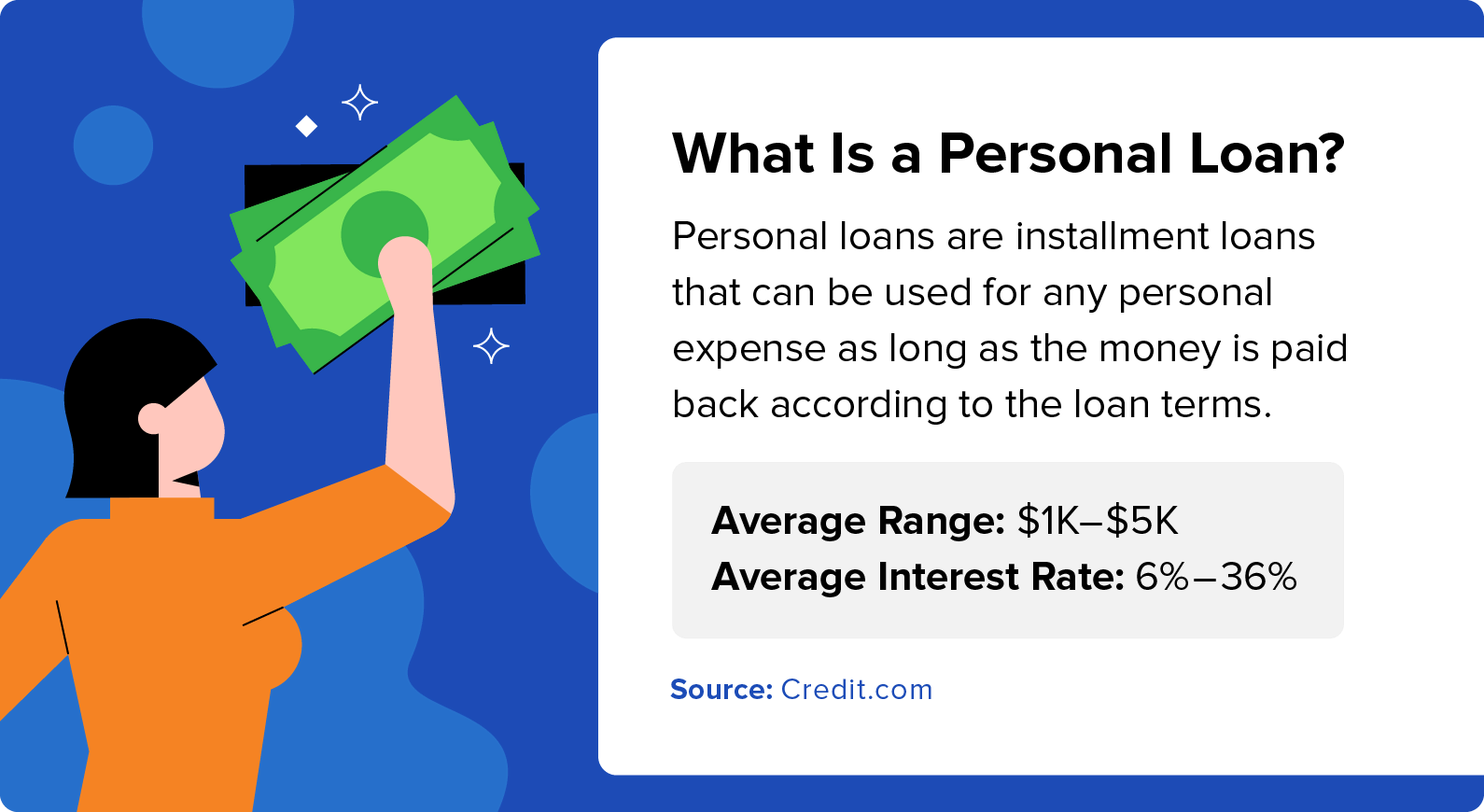

A personal loan is money borrowed from a bank, credit union, or other financial institution that can be used for virtually any personal expense. Like any other installment loan, personal loan borrowers are expected to pay the money back over a set period.

The amount you can take out for a personal loan can range anywhere from $1,000 to $50,000, depending on several factors. Interest rates are just as variable—they can be as low as 6% and as high as 36%, depending on your unique financial situation. The current average interest rate for personal loans is 12.35% as of September 2024.

If you’re planning on making a big purchase, getting a better handle on your debt, or have run into some unexpected expenses, applying for a personal loan can help cover the costs. People usually take out personal loans for:

Personal loans can also be a strategic financial tool in certain situations. Consider these three smart ways to use a personal loan.

While you could technically use a personal loan for anything, there are a few things you should avoid using a personal loan for, like:

Personal loans, personal lines of credit, and payday loans are all money-borrowing options that can help you manage your finances or cover a significant expense. However, they’re typically used for different purposes.

|

|

Definition |

What it's best for |

|---|---|---|

| Personal loan |

Supplies the borrower with a large sum of money upfront that must be paid back in fixed monthly payments throughout the loan term |

Large purchases or expenses |

| Personal line of credit |

Lets the borrower use credit as needed and pay it back on their own timeline with a variable interest rate |

Building credit on everyday purchases |

| Payday loan |

Gives the borrower a small sum of money—around $500 or less—at a high-interest rate that usually has to be repaid within 2-4 weeks |

Quick cash for urgent needs, especially if the borrower does not qualify for a traditional loan |

You have to receive a personal loan through an authorized lender, typically a bank or credit union. Here’s how the personal loan process works:

Note that while most personal loans do not have prepayment penalties, some lenders may impose them. If you plan to pay off your loan early, it's important to check the terms and conditions of the loan agreement to see if there are any associated fees.

Before you apply for a loan, research the type of personal loan that will best serve your unique financial needs. Your credit history, credit score, and reason for needing the loan will determine which is best for you.

Here’s a quick breakdown of the seven most common types of personal loans:

| Type of personal loan |

Definition |

Who it's best for |

|---|---|---|

| Unsecured personal loans |

Do not require any sort of collateral to qualify |

Borrowers with excellent credit and a steady source of income |

| Credit-builder loans |

Allow you to take out a small sum of money to demonstrate that you’re a reliable borrower by making regular on-time payments |

Borrowers with low or no credit history looking to improve their credit score |

| Debt consolidation loans |

Typically can be borrowed at a lower interest rate than most credit cards or other bills you plan to consolidate, saving you money on interest |

Borrowers with multiple debt balances or balances with high interest rates |

| Co-signed and joint loans |

Allow a co-signer to assume responsibility for a loan if the borrower does not qualify |

Borrowers who do not qualify for a traditional loan or are hoping to be approved for a lower interest rate |

| Fixed-rate loans |

Come with an interest rate that does not change over the repayment term, so the borrower pays the same amount every month |

Borrowers who plan on paying off their loan over an extended period |

| Variable-rate loans |

Come with a fluctuating interest rate that could increase or decrease monthly payments over time, but rates are sometimes lower vs. fixed-rate loans |

Borrowers who only need to borrow funds for a short period |

Personal loans are a great tool for financing some of life’s most important—and unexpected—milestones. If you’re ready to apply for a personal loan, follow these steps:

1. Check your credit: Your credit history will be the biggest determinant of whether or not you're approved for a loan, so it’s important you know where you stand. Most lenders will want to see a “good” credit score (620) or above to ensure you can be trusted to meet your loan terms.

2. Decide how much to borrow: You may qualify for a $50,000 loan, but before you sign on the dotted line, you need to know how much you can realistically afford to borrow. Carefully consider your current and future financial situation before jumping into any personal loan.

Pro tip: Try our loan payment calculator to easily estimate monthly payments for different personal loan options.

3. Know your consumer rights: According to the Truth in Lending Act, lenders must disclose the APR finance charges, principal amount, and any fees and penalties associated with a loan offer. If you come across a lender that refuses to share this information, you’ll want to look for a different lender.

4. Gather essential documents: In addition to your credit report, potential lenders may also want to see the following documents to speed up the application process:

5. Research loan options: Personal loan requirements and terms vary by the type of loan and lender, so you'll want to research before applying. Details that may sway your decision include the loan amount, APR, monthly payments, loan term, secured or unsecured, and more. Ask lenders for this information in advance before applying for a personal loan.

6. Submit your application: Once you’ve settled on a loan that meets all your requirements, fill out your application, read it carefully for typos or errors, and submit it to your potential lender. You’ll likely know whether your application was approved within a day or two whether your application was approved.

Each lender is different, so minimum requirements for personal loans vary. However, if you’re hoping to qualify for a large unsecured personal loan with a competitive interest rate, here are a few general requirements most lenders will want to see:

Again, these requirements vary from lender to lender. In some cases, you may qualify for a loan with no credit at all. Some lenders even prioritize things like education and work history when evaluating applicants. Inquire with potential lenders before you apply for a personal loan to better understand what you need to qualify.

If credit history, high interest rates, or substantial fees are preventing you from applying for a personal loan, there are money-borrow alternatives that may be a better fit, like:

Still weighing your personal financing options? We answered some of the most frequently asked questions about personal loans to help with your decision.

Applying for a personal loan may cause a light dip in your credit score because lenders will run a hard inquiry on your credit. While a hard inquiry shouldn’t affect your credit score too much, it’s important to narrow down your options before applying to avoid multiple hard inquiries from multiple potential lenders.

It’s also wise to wait to apply for a personal loan if you’ve just opened another line of credit, which could cause an even bigger drop in your score.

You do not need a down payment for a personal loan. However, In the case of a secured loan, you’ll need collateral, such as a car or money in a savings account.

You’ll likely be able to borrow upward of $100,000 with a 700 credit score, but other factors, including your income, employment status, and the type of loan you're applying for, may also impact how big of a loan you qualify for.

While there's no limit on applying for multiple personal loans, having too much existing debt can make it harder to qualify for future loans or lines of credit. Lenders consider your overall financial picture when making approval decisions.

Researching personal loans can be daunting, especially if you’ve run into sudden unexpected expenses. The best loan for you will depend on your unique financial situation. Check out the personal loans at Credit.com to quickly compare options and see potential APR, terms, and maximum loan amounts.

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.