It's Financial Literacy Month: Here's What Your Credit Score Wants You to Know

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Published November 26, 2018

While many parents consider the financial implications of having children, they don’t always consider the importance of family discussions about finances. Having at least a basic understanding of personal finance is crucial for success in life. Eighty-seven percent of Americans agree that financial literacy should be taught in schools. Unfortunately, the reality is that few states produce financially literate high school graduates. A survey conducted by Chase showed that only one third of Americans were taught what a credit score is by their parents! So it’s up to parents to bridge the gap.

If you’re a parent, don’t worry — it’s easy to teach your kids simple money lessons. Even providing the most basic lessons like budgeting and building credit go a long way.

This guide covers the basics of how to teach your teen and young adult kids about credit to set them up for a healthy relationship with their finances, including:

There are things you can do even before your child reaches high school to ensure that they start off on the right foot with credit. There’s no hard and fast rule for if and when you need to do these things, so if you haven’t yet, use this as a first step in the right direction.

Unless a child is an authorized user or joint account holder on an adult’s account, he/she won't have a credit score. Even so, the Federal Trade Commission recommends checking a child’s credit score around the child’s 16th birthday. This lets you correct any issues that may be caused by identity theft before your child turns 18 — the age when most of use first use and need a credit score.

To check your child’s credit report, send your written request to each of the major credit reporting agencies with:

Child identity theft has become increasingly common in recent years. Because kids' data is a “clean state” and not being checked regularly if at all, thieves are more likely to prey on it. To reduce your child’s risk of identity theft, be aware of common warning signs and check your child’s credit score every six to 12 months.

A Javelin Strategy & Research report, the 2018 Child Identity Fraud Study, showed why identity theft among children is a concern:

If your child’s identity is stolen, the sooner you discover the problem the better. If you suspect a problem or notice any of the warning signs listed below, contact the major credit agencies for more information. Warning signs of fraud include:

Freezing a child’s credit is the best way to prevent identity theft. Parents, legal guardians or someone with power of attorney can place a security freeze on the credit reports of minors under the age of 16. And now, thanks to changes to the Dodd-Frank law, freezing and unfreezing you or your child’s credit at each of the three credit bureaus (Equifax, Experian, and TransUnion) is free.

If you want to request a freeze (or unfreeze), check out tips on how to talk to a credit bureau before contacting the bureaus.

Knowledge is the most basic element of good financial health. The most important thing to do is to educate your kids on how to use credit as a financial tool. Focus on the positive aspects of having a good credit score, while emphasizing that access to credit is a serious responsibility with the potential to cause lasting effects if used recklessly.

Credit lets you and your kids “buy” goods or services before you actually pay for them, because you’ve proven that you can be trusted to pay in the future. Having good credit is important, because it’s used by lenders to decide to give you any type of loan, from big purchases like houses and cars to credit cards, cell phone contracts, renting an apartment and even getting a job.

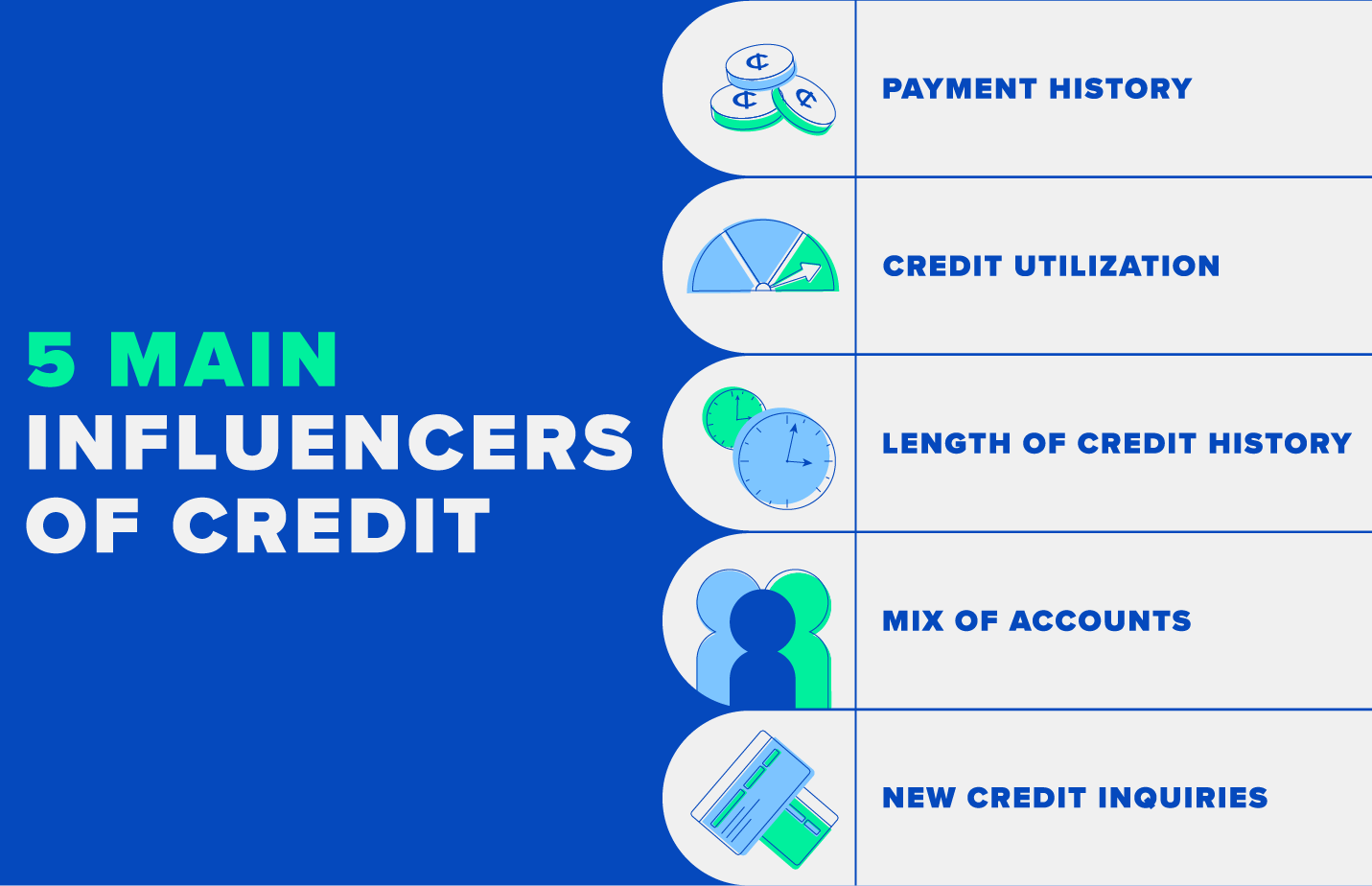

Teaching your child what impacts their credit history is a good place to start teaching them about credit.

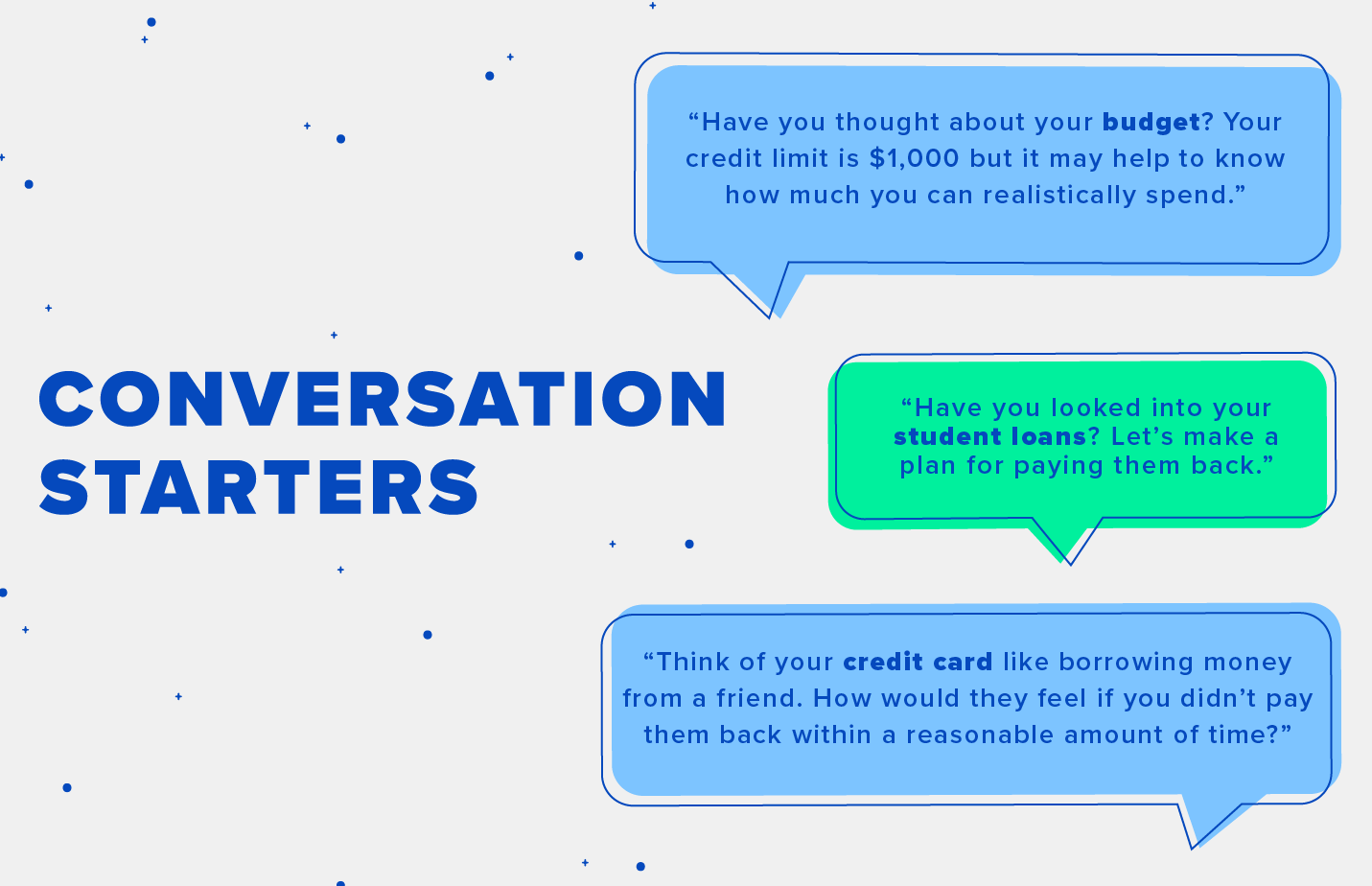

When you talk to your child about money in everyday conversations, you can boost your child’s financial literacy without even sitting down to discuss big topics. A 2014 study by the Federal Reserve showed that people in states that mandated financial education have higher average credit scores as adults than people in states without this requirement. Odds are that there are some aspects of your monthly routine, like paying bills or checking your own credit score, that can become teachable moments for your kids. It can be helpful to have a real-world connection to draw from when you talk to your kids, so pull from your own experiences when offering offer one of these lessons.

While there are money lessons your kids benefit from learning before high school, it’s never too early to teach the benefits of properly managing money. As your child approaches adulthood, it’s important to talk to them about credit and the many ways it affects their lives. Once they enter high school, you should to explain the basic concept of credit and start informing them of how actions, like paying the cell phone bill on time, impact credit scores and why that matters. Providing real-life examples is the best way to educate kids on a concept that is somewhat abstract.

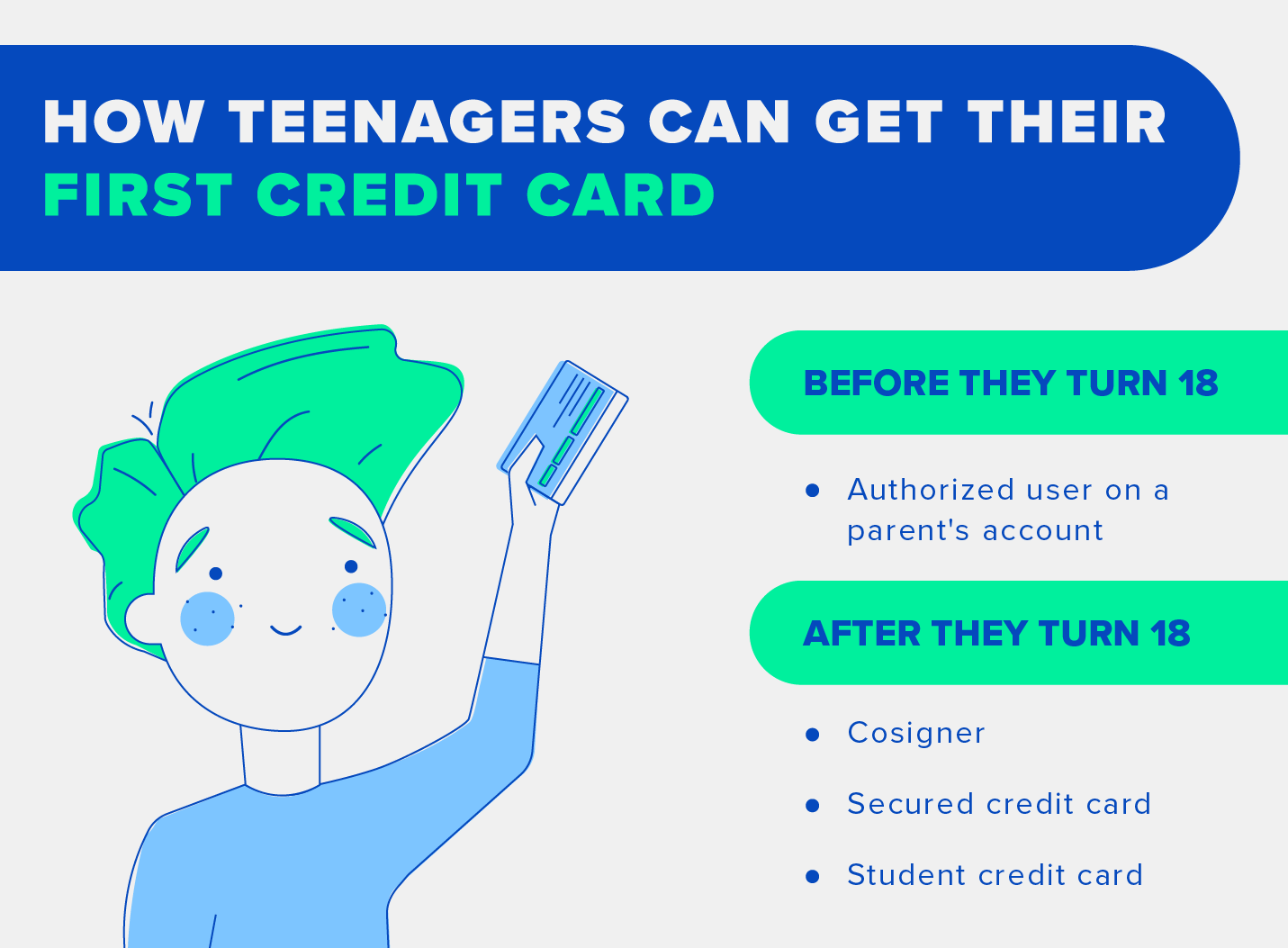

In 2017, T. Rowe Price’s annual Parents, Kids and Money Survey found that the number of children ages 8 to 14 with access to credit cards had quadrupled in just five years. If you’re wondering whether you can get your teen a credit card, technically, children under age 18 can’t apply for a credit card as the primary account holder. However, you can add minors to your own account as authorized users if and when you feel they’re ready. When to give your child credit card access, is a personal decision for every family. When you’re ready, here are a few ways to go about it.

There are several credit cards that are great for families. If you’re looking for a card that offers the best benefits for families, consider one of these:

It takes time to build credit, but once your child has access to a credit card, he/she can start. In addition to using a credit card responsibly, there are a few more ways your child can establish good credit. And, once your child has started establishing credit, encourage him/her to monitor one of his/her credit scores, which can be done for free.

Building credit takes time, but if your child starts early and practices good habits, he/she can establish a solid history with just 6 to 12 months of on-time payments.

Building credit isn’t always smooth sailing. Watch for signs that your child might be struggling financially. Ruining his/her credit can cause him/her to struggle finding a place to live or even a job. It’s best to intervene early. There are a few ways you can help if things have already taken a turn for the worse, including:

For some teens, college is their first real experience with credit. Realistically, college students have more to worry about than their credit, so it may not be top of mind. Even so, college is a great time for kids to start building healthy financial habits independent of their parents. It can seem as though credit won’t affect students until later in life, but remind your child that credit can impact them sooner than they might think. Here are a few things you want your kids to be aware of at this stage of life.

Paying for college with a credit card is never a good idea. Using student loans, though, is a standard way to pay for college these days. Federal student loans don’t require a credit check or cosigner, which means borrowers can take on large amounts of debt with little or no indication that they can pay it back, unlike credit cards. However, if your child hasn’t considered the effects of credit before, a student loan can lead to major sticker shock at graduation. Some things your child should know before taking out a student loan include:

College graduates have their own set of things to watch out for with regards to credit. As long as you’ve followed these tips though, you can feel confident that your new graduate is responsible and can make his/her own decisions once graduated and is on the way to getting a job.

If you’re nervous about starting the credit conversation with your child, consider that 41% of all households carry some sort of credit card debt. You may feel uncertain about your own finances, unqualified to teach about a concept you’re struggling with, or like you’re protecting your children by not introducing them to credit. We all know the “do as I say, not as I do” method of teaching isn’t the most effective, but for as many reasons as there are for not teaching your kids about credit, there are always more in support of it.

Sources: CNBC | Investopedia | The Balance | T. Rowe Price | Federal Reserve

Learn how to improve your credit score with essential tips on payment history, credit utilization, and more this Financial Literacy Month.

Learn how to use your tax refund to improve your credit score with these strategic financial tips. Boost your financial health and achieve your credit goals.

Take control of your financial health and strengthen your money relationship with practical tips to improve your credit score and set financial goals today.